Insurance market for affordable housing

Understanding trends and navigating a difficult insurance market

Gibbs Laidler Consulting LLP (Gibbs Laidler) are a firm of independent insurance consultants, specialising in the social housing sector. Established in 1997 and now retained by some 140 social housing clients across Scotland, England and Wales, Gibbs Laidler have assisted the below commonly known Housing Associations recently in Scotland:

As part of Gibbs Laidler’s service, we have assisted the above, and indeed all of our clients, with both their tender and renewal processes for many years. Gibbs Laidler assist with some 30 insurance tenders per year, and perhaps have the most detailed knowledge of the insurance market regarding social housing risks.

From around 2022, the majority of Scottish housing associations started to see signs of a hardening insurance market for their property-based risks; two years on, and the majority of associations are still feeling the effects of these market conditions, citing that their latest renewals are:

For this reason, insurance is starting to be escalated up the agenda on many association’s risk registers, with some associations noting that their risk register includes not being able to procure insurance at all (or at least for a sustainable premium).

Amongst the many SFHA members who have mentioned newfound struggles with insurance, some common trends have been apparent. On this basis, the SFHA have asked Gibbs Laidler to provide their perspective on these trends, with some potential solutions on how to best mitigate the effects of these difficult market conditions where possible.

Therefore, Gibbs Laidler, interviewed a number of Scottish housing associations from different regions of the country, combining this with their learned knowledge of their retained clients to produce the following observations.

As may be common knowledge, the insurance market for housing associations is fairly small when compared to the insurance market which may be available for private property owners. This is perhaps because of the unique nature of a housing association’s core activities, and the scale of their operations, typically owning or factoring for hundreds or even thousands of properties.

At the same time, there have been some large claims within the sector, which have perhaps caused a hesitance from prospective insurers to underwrite new business within the sector, or at least to compete with the historic rates that associations might typically have seen. Some reports suggest that rates for private property owners might commonly be circa three or four times higher than rates that might have been typical for associations around 2021, and on this basis there have only been a limited number of insurers willing to underwrite property risks for housing associations at such premiums.

From Gibbs Laidler’s discussions with members, the main available insurance providers for property risks appear to be:

Of course, insurance brokers may likely have access to a number of different insurers, and on this basis there may be a number of different property insurers (at the time of writing) available to Scottish Associations via brokers including:

However, the key issue here is that due to exclusive arrangements between certain insurers and brokers, no singular insurance provider can obtain quotes from the entire insurance market. Therefore, the main impact here is that to be certain an association has engaged as much of the available insurance market as possible, they must likely consider an independent full market tender. Otherwise, the association must accept that they will perhaps have limited access to an already limited number of available insurers, and that these insurers may or may not have appetite for their property risk.

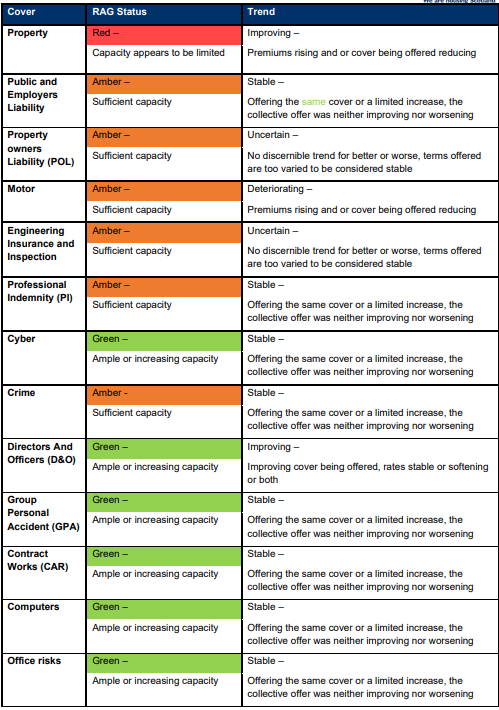

Therefore, across the different insurance markets which members typically reported on, this appeared to leave each policy, from Gibbs Laidler opinions, as follows:

The table illustrates the current insurance market, with a focus on choice of insurers, the competitiveness of premiums and whether the insurance cover is improving or worsening. We assessed thirteen individual classes of Policy cover based on insurer capacity for that particular line of business, using a RAG (Red, Amber, Green) status. Markets rated ‘Green’ appeared to have ample or increasing capacity, ‘Amber’ had sufficient capacity and ‘Red’ in cases where capacity appears insufficient for demand.

Of the thirteen classes:

We then further classified the lines of cover based upon trends we have observed in the last few months. Those with an ‘Improving’ trend would have improving cover being offered, with premium rates stable or softening, or both. A ‘Stable’ trend would suggest insurers for that cover were asking for a similar thing repeatedly (e.g. a limited rate increase or offering the same cover) but the collective offer was neither improving nor worsening. A ‘Deteriorating’ trend would be where premiums are rising and/or the cover being offered is reducing, an ‘Uncertain’ trend is one where there is no discernible trend for better or worse, but terms offered are too varied to be considered Stable.

Of the thirteen classes of Policy cover:

From the associations which Gibbs Laidler spoke to, it also appears that there has been some reduction in cover which insurers have been able to offer. Typical reductions in cover appear to include:

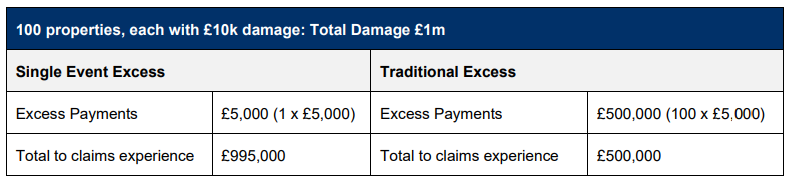

Some insurers may still offer a single-event excess, however this is one element of cover that other insurers have started to remove, in an attempt to keep premiums at stable levels.

Limited cover of certain buildings. Perhaps a growing trend amongst members, some associations have found that where some insurers are particularly unkeen on certain buildings (say due to the construction type), restrictions of cover have been placed on these buildings. During the interviews with Gibbs Laidler the most restrictive cover limit seen appeared to be a £5m capping to a building with a total rebuild value of c.£20m. This left the particular association with a £15m exposure which required an additional insurance policy (only confirmed post-renewal) to ensure this exposure was not on the associations balance sheet.

In addition, some SFHA members had seen their insurer impose similar terms in the absence of detailed construction information, with some associations, whilst not yet limited in cover, being given a time limit to provide this level of detail. These members reported that if this deadline was not met, the insurer would start to impose similar cover restrictions to the above, until further information can be provided.

Restrictive Storm/Flood Terms. Similar to the removal of single event excess, due to changing climate conditions, it is no secret that insurers are starting to become more aware of the risk presented by storm and flooding events. This is because, these events are by nature catastrophe-style incidents and are to some extent unavoidable. From the conversations that were held, a number of members reported their insurers undertaking “geospatial mapping” to understand the exposure which their portfolio might have to storm and flood events.

Where there were particularly high concentrations of stock in high risk areas, it seems that insurers would either price in more premium to cover this exposure, or adjust the insurance terms (say an increased excess), to provide some limit to their exposure.

From the associations which Gibbs Laidler spoke to, c.25% had experienced a significant flood or storm claim in recent years. Yet, it was only clear that perhaps one or two associations had actually seen the modelling data which their insurers had used, or undertaken a similar project themselves.

The issue here is that with the changing climate, areas which might not have been a historic flood or storm risk, might now start to see greater rainfall, windstorms or flooding. As an example, surface water flooding (pluvial flooding) occurs where drainage systems are overwhelmed by heavy rainfall; where perhaps historically associations had never experienced any events which might have overwhelmed these systems, this is starting to become more frequent across the UK, with areas that were always understood to be unlikely to flood causing significant losses for insurers. Therefore, some members had reported seeing that their insurers had adjusted the cover they were prepared to give based on this modelling data, not necessarily driven by historic losses, but due to the forecasts of where significant events may occur in the future.

Introduction of the average clause. Fundamentally speaking, the average clause is a clause in most insurance policies which allows insure to reduce claims payments if it transpired that the property is underinsured. This is a common clause amongst most commercial insurance policies, however the social housing property market has typically enjoyed the benefit of insurers waiving this clause, providing there is no intentional underinsurance.

However, some members reported that during their last renewals, where their property stock had not been professionally surveyed their rebuild values, that their insurers (albeit in varying ways) had started to re-introduce the average clause until a formal revaluation had been completed. Following this, it appears members are now instructing surveyors to assist them with these rebuild cost assessment projects. Of the associations Gibbs Laidler spoke to, c.65% of associations had reported having a professional survey in the last two years, which gives perhaps gives insurers (and more importantly associations), some piece of mind that their declared values are adequate.

However, it is perhaps important to understand why insurers may need to adjust their insurance terms:

Whilst the premium for the property stock was the largest expenditure for members, they also reported that there are a number of other policies where they have seen changes from their insurance providers.

As per the table of markets, we have picked the top 3 ancillary policies that were raised as points of concern for members:

1) Liability Policies (Property Owners, Public, Employers)

From speaking with members, a number of members had noted seeing increased liability premiums. Many members cited that these premiums had jumped up, despite them only making a relatively small number of claims on these policies. For most, natural growth (increases in wage roll, turnover etc) will account for much of these premium increases. In addition: some uncertainty surrounding court award costs, large claims within the entire social housing sector, and additional claims regarding areas such as damp & mould have all caused insurers to reassess the rates at which they are underwriting liability properties.

2) Motor Fleet

The insurance market for motor fleets have started to become more volatile.

Fleet policies are largely underwritten based on the claims experience, so those fleets that are unfortunate enough to experience large volumes of claims, will to some description be open to market pressures at each renewal. In addition, the average cost of a motor claim, according to the Association of British Insurers rose 8% to some £4,800 per claim. There are many potential reasons for this however, some key justifications include:

The result of this, is that insurers have had to increase rates, and in turn many members have started to receive largely increased premiums. On average this looked like some 35% for poorly performing risks.

Yet, for those well-performing risks, Gibbs Laidler noted that a number of fleet policies may offer premium rebates to members, resulting in some associations receiving lucrative rebates at the end of the policy year.

3) Cyber

The cyber insurance market continues to be difficult to navigate for the entire social housing sector. Insurers have taken significant losses in recent years, with some major incidents reportedly running into the millions of pounds. The sector is now unfortunately in a position where underwriters wish only to competitively underwrite the “best risks”, where security systems are most durable, and some associations are still on a journey to provide the required level of security. For a cyber policy, coverage typically may be arranged on either an “any one claim” or “aggregate” basis:

For those associations who might not yet have been able to integrate all of the insurer’s required security systems, some members, along with comparable cases throughout the UK have either:

For the most part, we have explored the current position of the insurance market for housing associations. However, each member that was interviewed asked for some comments on how the insurance market might change in the foreseeable future.

This is of course a purely speculative topic, and will be dependent on some key factors such as:

Yet, there are some initial signs that the next 24 months might bring some positive change. A small proportion of members reported seeing very similar premiums to their existing levels, with some tenders returning three or four quotes, where perhaps two proposals might have been considered a pleasing result.

Some insurance professionals might now also say that as rates and premiums have now increased, these might eventually be lucrative enough for prospective insurers to join/rejoin the market, bringing some degree of competitive pressure back into the market. However, it is generally accepted that this can take time to happen, and the positive effects might take up to 24 months to be felt holistically by the sector.

During our research several associations asked if now was the time to consider alternative insurance options such as:

This was in view of the hardening market conditions causing increasing premiums and cover restrictions. As with any type of alternative risk transfer, this comes down to what we might call the central issue:

“In order for alternative risk financing to be beneficial, you must be able to fund all of the loss costs, as well as all of the ancillary costs, and protect your organisation against unexpected losses and future liabilities, for less than the amount which you would pay for conventional insurances.”

For the majority of associations, there will be a lending/funding agreement in place for their properties; therefore this might initially restrict the ability to explore some of these options, and might perhaps then only lend itself to higher excesses.

In addition, claims by their very nature are unpredictable. Therefore, if for example, an association was to choose not to insure certain elements of their stock, they run the ultimate risk of having a total loss of a property which is not insured, and therefore the whole cost will be borne by the Association. For those associations with large accumulations of properties, a storm, flood, or fire might create a costly event, which if not budgeted for correctly by the association could come with major financial impact.

Therefore, given our experience of the insurance market for social housing risks, the conventional insurance market appears competitive enough for the majority of members to satisfy the central issue. However, we would advise that each association be aware of these alternatives, in the case that they appear feasible and can be moved to as part of a long-term strategy.

To summarise, Gibbs Laidler’s research with members would suggest that the last two years have proved to be a turbulent time for most insurance programmes, with many associations seeing increased premiums and/or restricted insurance cover. This is indeed no different to the experience of other housing associations across the UK, and are underpinned by similar issues and insurer behaviours.

Yet the insurance market is not impossible to navigate, and although currently this is relatively small with regards to the number of providers, there are some positive stories amongst members which we hope will increase in the foreseeable future. However, for now at least, it is perhaps important for associations to keep their options open, and paint the clearest picture of their risk to both their incumbent and prospective insurers using the data they provide.

We hope you find this report to be a comprehensive summary of our research and findings. If there are any questions, please do not hesitate to contact one of the below:

Nathan Hoskins

Andy Bygrave